Full name

Jan. 11th, 2022

◆

5 min read

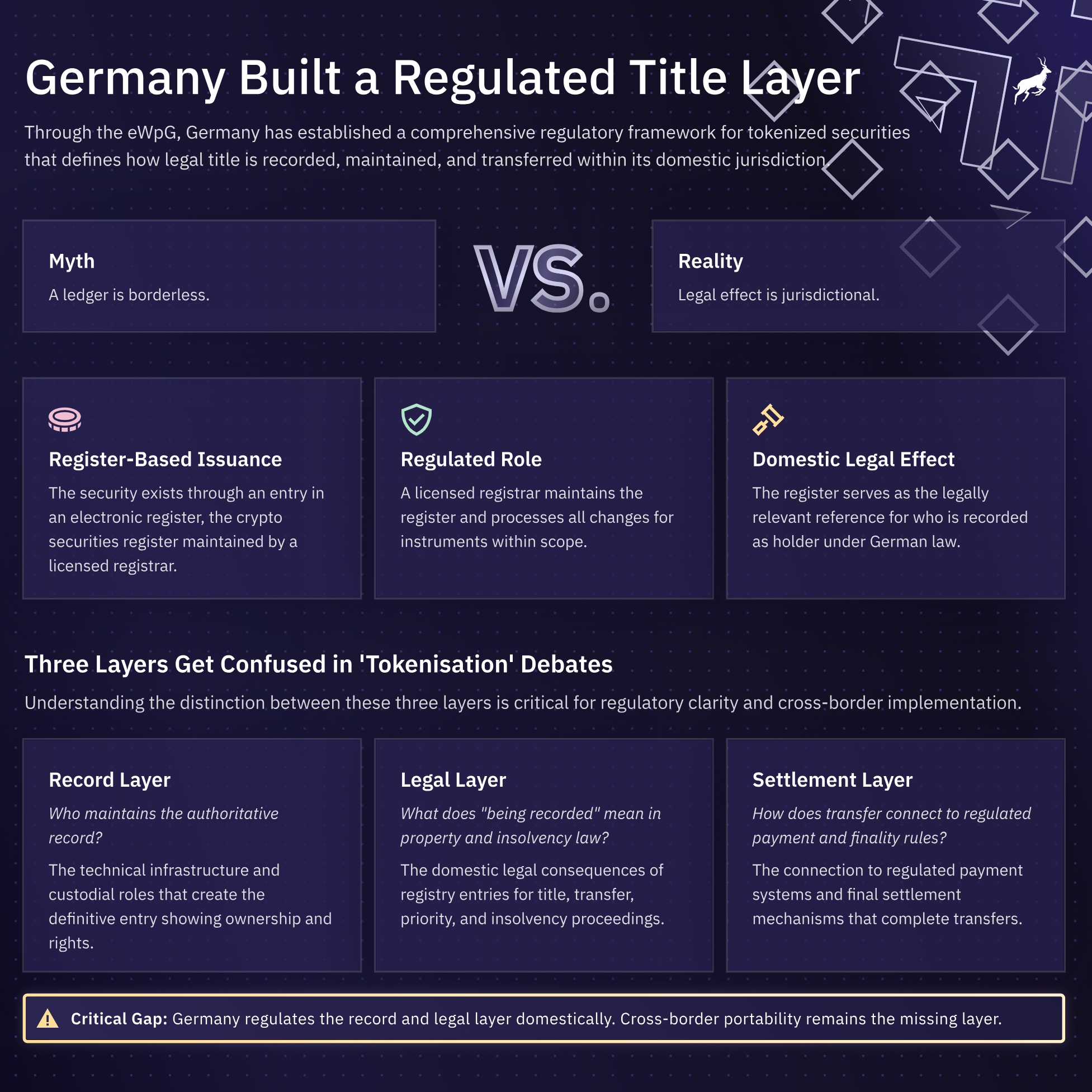

Germany's Electronic Securities Act (eWpG) answered a basic question: What happens when the paper certificate disappears? An electronic security exists through an entry in an electronic securities register. The holder is whoever that register names. Property law questions follow the law of the state supervising the registerkeeper. This creates domestic certainty. It also creates a border. A German register entry carries German legal effect, not automatic EU-wide recognition.

The EU's Market Integration Package, presented on 3 December 2025, targets capital markets fragmentation. COM(2025) 943 proposes permissions for DLT notary and central maintenance services within the DLT Pilot Regime, mapped to CSDR concepts. Cross-border viability turns on legal effect, perimeter definitions, supervision, and settlement interfaces.

The eWpG states that a security becomes an electronic security through entry in an electronic securities register. No paper needed. The register entry is the instrument itself.

The eWpG defines the holder as the person named in the register. The register is legally decisive, not just operationally convenient.

The eWpG treats electronic securities as "things" under the German Civil Code (BGB). Investors get property-law protection, not just contract-law promises.

The eWpG distinguishes central registers from crypto securities registers. Section 16 requires tamper-resistant systems for the latter. Law stays technology-neutral. Supervisory practice confirms DLT compatibility for issuance.

BaFin licenses crypto securities registerkeeping under the Banking Act. Duties cover investor protection and market integrity. Registerkeepers become supervised infrastructure, not tech vendors.

The eWpG contains the precise explanation. It includes a choice-of-law anchor.

The eWpG provides, that rights in electronic securities and dispositions over them follow the law of the state supervising the registerkeeper where entry occurs. Domestic actors know which property law applies. Cross-border investors know the anchor jurisdiction. No automatic EU portability.

Cross-border cases raise familiar questions.

Which law governs title and transfer across Member States?

What happens to register records in insolvency?

Will other jurisdictions treat German register entries as decisive for priority or enforcement?

Without EU harmonisation, cross-border use cases need extra legal engineering.

2.3 Market workarounds

Jurisdiction-specific opinions. Duplicate roles. Conservative structures. Register-to-books reconciliation. Legal fragmentation forces operational complexity.

The Commission frames EU capital markets as underdeveloped. Stock exchange market capitalisation sits at 73 percent of EU GDP versus 270 percent in the US.

Factsheets highlight simplified CSD processes, settlement system links, and relaxed DLT limits. DLT becomes part of market infrastructure integration, not an isolated experiment.

The reason DLT notary services matter is simple. "Notary" and "central maintenance" aren't new. They're defined CSDR post-trade functions that already carry legal weight.

CSDR's Annex sets out three core CSD services: initial recording in book-entry form (notary), maintaining top-tier securities accounts (central maintenance), and operating settlement systems. COM(2025) 943 doesn't invent these categories. It unbundles them for DLT execution.

The proposal creates individual permissions for entities to provide DLT notary service or DLT central maintenance service. Investment firms, regulated markets, banks, CSDs, and CASPs can apply. These permissions explicitly reference CSDR Title III requirements. ESMA gets the technical standards job, specifying which CSDR rules apply to distributed models and how.

Most important: the venue compliance bridge. An EU issuer whose DLT instruments trade on regulated venues satisfies CSDR book-entry rules when the securities live on a distributed ledger maintained by a permitted DLT notary. That's actual legal engineering.

Want to know if registrar-style functions scale EU-wide beyond trading venues? The German model and EU proposal answer differently across five dimensions.

Legal effect lives in the register, jurisdictionally anchored: Germany's eWpG makes this explicit – effect follows supervisory state law. EU portability needs cross-border recognition rules that actually work in conflict and insolvency scenarios.

Perimeter draws hard lines: COM(2025) 943 covers DLT instruments on trading venues. Primary issuance to EU investors or OTC/collateral workflows? Those sit outside the explicit language.

Supervision splits national from EU competence: The Commission factsheet hints at stronger ESMA roles. COM(2025) 943 formalises ESMA's standards role. But who actually intervenes when a cross-border problem hits?

Settlement finality stays regulated: CSDR treats settlement as the third leg. COM(2025) 943 permits unbundled issuance/recording outside CSDs but keeps settlement infrastructure regulated. Register changes still need a bridge to settlement finality.

Joint provision demands contractual clarity: Multiple entities handling core services? COM(2025) 943 requires binding agreements allocating every role and liability question. Models live or die on these arrangements.

COM(2025) 943 can map DLT notary/maintenance to CSDR obligations via ESMA standards, but portability remains a private-law problem. The market will continue to rely on opinions, structuring, and layered post-trade arrangements until recognition mechanisms and conflict-of-laws treatment are addressed at EU level.

Book a call with our expert.